How to Get a Centurion Card Invitation 2026

There is hardly a credit card topic that generates more speculation than the invitation to the Centurion Card. In forums and Reddit threads, you read everything: fixed spending thresholds, secret algorithms, magic spending categories. Some of it is roughly correct. Much of it is wrong. And some of it is so absurd you wonder where people get their information.

I received the invitation. I have held the card for several years. What I am writing here is based on my own experience and on conversations with other Centurion cardholders. No rumors. No third-hand hearsay.

Myth vs. Reality

Let's start with the most persistent myths.

Myth: There Is a Fixed Spending Threshold

The most widespread myth: you have to spend exactly 250,000, 300,000, or 500,000 euros per year on your Amex cards, and then the invitation automatically arrives. The number varies depending on who you ask.

The reality: there is no official, fixed threshold. American Express has never stated a specific number and will not do so. What I know from personal experience and conversations: annual spending plays a role, but it is only one factor among several. The range that realistically leads to an invitation starts at around 250,000 euros and up. Some cardholders report less, others significantly more. There is no switch that flips at a certain amount.

Myth: You Can Apply

You regularly read that you can call Amex and ask about the Centurion. Or that you should signal to your Relationship Manager that you are interested. The idea: if Amex knows you want the card, it speeds up the process.

The reality: you cannot call and apply. The Centurion Card is an invitation-only product. Period. There is no application form, no waitlist, no "please make a note." Whether a conversation with the Relationship Manager helps is unclear. My personal assessment: it probably does not hurt, but it does not help much either. The decision is made at a different level, based on data, not requests.

Myth: A Large Single Purchase Triggers the Invitation

Some believe that a particularly large single transaction, a car, an expensive watch, a deposit on a property, would trigger the invitation. The logic: Amex sees the big transaction and thinks "this person can afford the Centurion."

The reality: single transactions are irrelevant. What matters is the pattern over time. A one-time purchase of 50,000 euros impresses no one at Amex if the rest of the year sits at 2,000 euros per month. Consistency matters more than peaks.

Myth: Certain Spending Categories Are Decisive

In some forums, it is claimed that Amex pays special attention to travel and restaurant spending. The theory: those who travel a lot and dine out frequently fit the Centurion profile.

The reality: this is one of those myths with a kernel of truth. Amex does indeed look at spending patterns, not just the total. A cardholder who spends 300,000 euros per year on travel, hotels, fine dining, and upscale retail fits the Centurion profile better than someone who runs the same amount through a single wholesale supplier. This does not mean you should artificially redirect your spending into certain categories. But if your natural spending behavior already trends in that direction, it is a positive factor.

What Actually Matters

Based on everything I know, Amex evaluates invitation candidates on several factors. None of them is decisive on its own.

Annual Spending Across Amex Cards

Yes, spending counts. It is probably the single most important factor. But it is total spending across all your Amex cards, not just one. If you use a personal Platinum and a Business Platinum for work, both feed into the picture.

The ballpark: 250,000 euros and up as a rough benchmark. Some cardholders report being invited with less. Others have spent more for years and were never invited. Spending alone is not enough.

Length of the Customer Relationship

Amex favors long-standing customers. Someone who has had a Platinum for two years and suddenly spends a lot is in a different position than someone who has continuously used Amex cards for eight or ten years and gradually increased spending over time. The card history shows Amex that you are a stable, long-term customer, not someone generating short-term volume to force an invitation.

My path: I was an Amex customer for over seven years before the invitation came. First Gold, then Platinum, then Business Platinum. Each card held for years, never canceled.

Payment Behavior

This sounds basic, but: pay your bills on time. Always. Without exception. A cardholder who regularly falls behind or uses installment payments will not be considered for the Centurion. Amex looks for customers who settle their statements in full and on time.

Spending Patterns

As already mentioned: the type of spending matters. A diversified spending profile with emphasis on travel, dining, and upscale retail fits the Centurion customer profile better than concentrated spending in a single category.

Overall Relationship with Amex

Do you hold multiple Amex products? Do you actively use Membership Rewards? Have you redeemed Amex Offers? Do you book through Amex Travel? All of these data points contribute to the picture Amex has of you as a customer. The more deeply embedded you are in the Amex ecosystem, the more likely you are to be identified as a Centurion candidate.

What Definitely Does Not Help

A few things I keep reading about that demonstrably do not work.

Calling the Hotline and Asking

Several people have told me they called Amex and asked about the Centurion. The staff response is always the same: polite but firm. The Centurion is an invitation product, there is no application process, they cannot arrange an invitation. You have gained nothing, except that your call may have been noted somewhere.

Artificially Inflating Spending

Some people deliberately buy expensive items through Amex and then return them to drive up card volume. This is not only pointless but counterproductive. Amex sees the returns. High gross spending with lots of chargebacks does not create a positive customer profile.

Reckless Spending

Increasing spending just to hit the Centurion threshold is financial nonsense. The Centurion is a tool for people who already spend a lot. Anyone who changes their spending behavior to get a credit card has their priorities wrong.

Applying Pressure Through Third Parties

There are reports of people who tried to advocate through their accountant, their banker, or other supposed contacts at Amex. This does not work. The invitation decision is made internally, based on data, not recommendations.

The Invitation Process

Once Amex has identified you as a Centurion candidate, the process unfolds in several steps.

The Invitation Letter

You receive a letter. Not by email, not by phone call. A physical letter. In my case, it was a high-quality letterhead in a black envelope introducing the Centurion Card and inviting me to membership. No glossy marketing, more understated and factual. That fits the card's self-image.

The Call

Shortly after the letter, two days later in my case, a Relationship Manager called. Not a regular customer service representative, but someone from a specialized team. The conversation was pleasant and pressure-free. He explained the terms, the costs, the benefits. He answered questions. He did not push for a close.

What pleasantly surprised me: the Relationship Manager was honest. He did not say the card is worth it for everyone. He said the card supports a certain lifestyle, and that I would be the best judge of whether that applies to me. This was not a sales pitch. It was a conversation between equals.

The Decision

After the call, I had a few days to decide. There was no ultimatum, no "this week only." The invitation had a validity period, but it was generous.

The Review

After I accepted, there was a brief review. Not an extensive credit check in the traditional sense. Amex already knew my financial situation from years of the customer relationship. More of a formal confirmation.

The Onboarding

The initiation fee and the first annual fee were due with the next statement. Just under 8,000 euros in the first year. No installment plan, no discount. Full price.

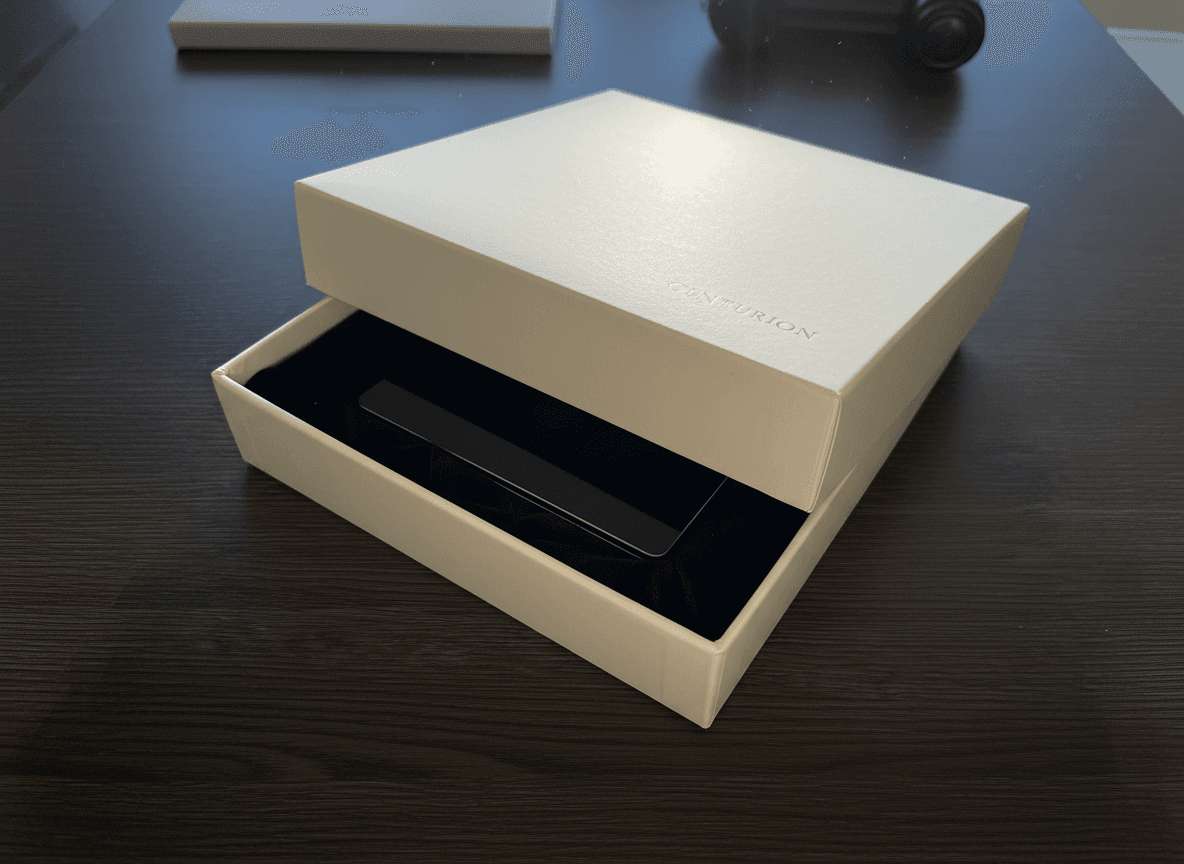

The Card Delivery

The card arrived about two weeks after confirmation. In a box far more elaborate than anything I had previously received from Amex. The titanium card itself has a noticeable heft and feels different in the hand than a regular credit card. It came with a welcome folder containing information on all benefits, contact details for the concierge team, and access to the online portal.

Was the unboxing impressive? Yes. Was it worth the price? The unboxing alone, certainly not. But it sets the tone for what the card aspires to be: not ordinary.

What Happens After the Invitation

The first weeks with the Centurion are a settling-in phase. You get to know the concierge, you test the various services, you notice where the card makes a real difference and where it does not.

My advice for new Centurion cardholders: use the first three months deliberately to try out all the services. Call the concierge, even for smaller matters. Book through FHR. Use the lounge access. That is the only way to get a realistic picture of whether the card fits your life.

After the first few months, you will know which services you use regularly and which you do not. And you will have a well-founded assessment of whether the 5,000 euros per year makes sense for you.

My Own Path

I rarely tell my personal story, but in this context it is relevant.

I started with the Amex Gold in 2017. Not because of the Centurion, but because I had started traveling internationally more frequently and needed the insurance benefits. After two years, I upgraded to the Platinum because the lounge access and the Fine Hotels & Resorts program made sense for my travel patterns.

The Business Platinum came a year later, when I began routing business expenses consistently through Amex. At that point, my combined annual spending across all Amex cards was roughly 180,000 to 220,000 euros. Not because I was trying to hit a specific threshold, but because that was my natural spending volume.

In the fifth year as a Platinum cardholder, the seventh as an Amex customer overall, my combined spending was around 280,000 euros. I had never asked about the Centurion. I had never altered my spending behavior to provoke an invitation. I had simply used Amex cards consistently as my primary payment method wherever they were accepted.

The letter arrived on a Friday. The call came the following Monday. I took a week, ran the numbers honestly to see whether the card made sense for my usage patterns. The math worked out narrowly. Not clearly, but narrowly. What tipped the scales was the concierge. I had used the Platinum concierge regularly and was mostly satisfied. The prospect of a significantly better service in that area was the deciding factor for me.

Looking back: the decision was right. Not because the card has paid off dramatically, but because it fits my lifestyle. It is a tool I use regularly. Nothing more and nothing less.

Summary

There is no hack, no shortcut, and no trick. The Centurion invitation is the result of a long-standing, active customer relationship with high spending and a spending profile that fits the Centurion customer segment.

What works: using Amex cards as your primary payment method. Consistently high spending over years. On-time payment. Diversified spending. Patience.

What does not work: calling and asking. Artificially boosting spending. Restructuring expenses just to stand out. Impatience.

And perhaps the most important insight: the question should not be how to get the invitation. The question should be whether the card fits your life. If the answer is no, the invitation is worthless. If the answer is yes, and your spending behavior matches, the invitation will come eventually. Without you having to force it.